If you run a small business and provide a car or vehicle to yourself, a staff member, or even a working director, you may be entering into Fringe Benefits Tax (FBT) territory—whether you realise it or not.

FBT on cars and other vehicles is one of the most common (and commonly misunderstood) areas for small business owners. It’s also a regular focus area for the ATO. The good news? With the right records and understanding, you can stay compliant and even reduce your FBT exposure.

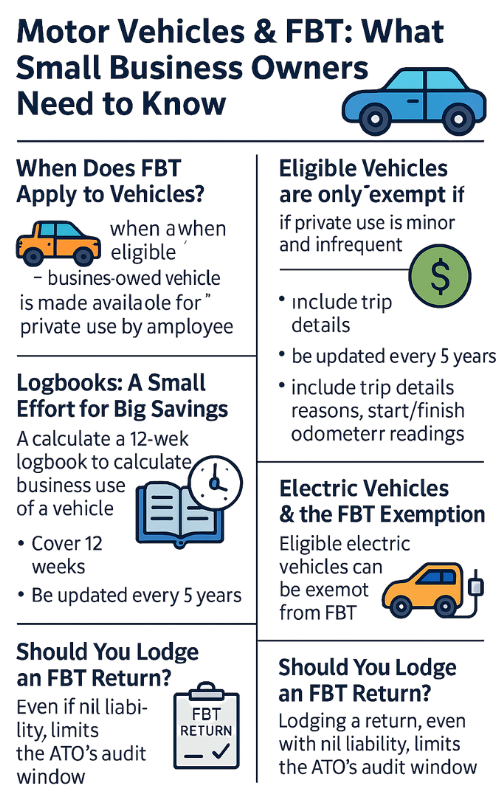

When Does FBT Apply to Vehicles?

FBT generally applies when a business-owned vehicle is made available for private use by an employee (including directors and family members). This includes even small amounts of private travel, like stopping at the shops on the way home.

“But it’s a ute—aren’t they exempt?”

A common myth is that certain utes, vans or dual cabs are automatically exempt from FBT. In reality, the exemption for “eligible vehicles” only applies if private use is strictly limited to minor, infrequent, and irregular travel.

If an employee uses the vehicle for regular private purposes—like weekend camping or the daily school run—the exemption likely doesn’t apply. To rely on it, you must show:

The vehicle is not principally designed to carry passengers (e.g. has a payload of more than one tonne)

Private use is limited and documented

A signed employee declaration and records of the vehicle’s use are essential here.

Logbooks: A Small Effort for Big Savings

One of the best tools for reducing FBT is a 12-week logbook. This helps calculate the business use percentage of a vehicle under the operating cost method.

A valid logbook must:

Cover 12 continuous weeks

Be updated every five years (or when usage changes)

Include trip dates, reasons, start/finish odometer readings, and distance travelled

You’ll also need odometer readings at the start and end of each FBT year (1 April to 31 March), and potentially employee declarations depending on your calculation method.

Electric Vehicles & the FBT Exemption

Thinking of going electric? There’s a valuable incentive: eligible electric vehicles can be exempt from FBT.

To qualify:

The EV must be a zero or low emissions vehicle

It must have been first held and used on or after 1 July 2022

The value must be under the luxury car tax threshold for fuel-efficient vehicles

Even when exempt, employers still need to do the usual paperwork—especially if there’s a reportable fringe benefit amount to be included on employee income statements.

Employee Contributions: Another Way to Reduce FBT

If you’d rather avoid or reduce your FBT liability without relying solely on logbooks, you can use an employee contribution.

This is where the employee reimburses the business for part (or all) of the private use value of the car. For example:

If the taxable value of the car benefit is $4,000, and the employee reimburses $4,000, your FBT liability is reduced to nil.

The reimbursement must be paid (not just journaled) by 31 March of the FBT year.

It is included as income for the business and may attract GST if you’re registered.

This method is beneficial for owner-operators, provided that proper payments are made and documentation is retained.

Should You Lodge an FBT Return?

Even if your FBT liability is nil, lodging a return can cap the ATO’s audit window to three years. Without it, the ATO can review your records indefinitely. It’s often a smart protective step.

Need Help?

If you’re unsure whether your vehicles attract FBT, whether a logbook or employee contribution would suit you better, or how to apply the EV exemption—chat with your accountant or tax adviser early. The right approach can save a lot of time, tax, and stress later on.

Let’s take the guesswork out of FBT. Reach out if you’d like help reviewing your vehicle policies or records this year.